[VOL.009] The Ultimate Guide to Canada’s Top Tax-Advantaged Accounts: TFSA, FHSA, and RRSP (2025)

Explore Canada's top tax-advantaged accounts—TFSA, FHSA, and RRSP—to optimize your financial strategy in 2025. Understand each account's features, tax benefits, and ideal uses to make informed decisions for your savings and investments.

Many Canadians struggle to navigate tax implications while trying to save for critical life goals, whether it's buying a first home, preparing for retirement, or building financial security. The complexities of tax planning can feel overwhelming. Fortunately, Canada offers powerful tax-advantaged accounts designed to help you keep more of your hard-earned money.

Comprehensive Account Comparison

Detailed Account Breakdown

1. Tax-Free Savings Account (TFSA)

The TFSA offers exceptional flexibility for short-term savings, long-term investments, or emergency funds.

Key Features:

Eligibility: Canadian residents aged 18+

2025 Contribution Limit: $7,000 (Unused contribution room carries forward)

Lifetime limit (2025): $102,000 for those eligible since 2009

Tax Advantages:

Non-tax-deductible contributions

Tax-free Investment growth and withdrawals

Ideal Uses:

Flexible savings for vacations, major purchases, and emergencies

Long-term investing with tax-free growth

Penalty-free withdrawals at any time

2. First Home Savings Account (FHSA)

Introduced in 2023, the FHSA combines the best features of TFSAs and RRSPs specifically for first-time homebuyers.

Key Features:

Eligibility: Canadian residents aged 18+ who haven't owned a home in the current or past four years

2025 Contribution Limit: $8,000 (Unused contribution room carries forward)

Lifetime limit (2025): $40,000

Tax Advantages:

Tax-deductible contributions

Tax-free withdrawals for a qualifying home purchase

Ideal Uses:

Accelerated savings for a first home

Maximized tax benefits while building your down payment

3. Registered Retirement Savings Plan (RRSP)

The RRSP remains Canada's primary retirement savings vehicle with additional benefits for homebuying and education.

Key Features:

Eligibility: Canadian residents with earned income

2025 Contribution Limit: 18% of previous year’s income (max $32,490)

Tax Advantages:

Tax-deductible contributions

Tax-deferred investment growth until withdrawal

Special withdrawal programs for homebuying and education

* Taxation on Withdrawals

When you withdraw from your RRSP (outside of the Home Buyers' Plan or Lifelong Learning Plan), your financial institution will deduct the withholding tax automatically:

10% on up to $5,000 (5% in Quebec)

20% on $5,001-$15,000 (10% in Quebec)

30% on over $15,000 (15% in Quebec)

* Special Programs

Home Buyers' Plan (HBP): Withdraw up to $60,000 tax-free for first home (Repayment within 15 years)

Lifelong Learning Plan (LLP): Withdraw up to $20,000 for education (Repayment within 10 years)

Ideal Uses:

Reducing taxable income in high-earning years

Retirement planning with potential access for homeownership or education

Strategic Use of These Accounts

Maximizing your savings and minimizing taxes often involves finding a balance that works for your financial situation. Here are some ways to consider combining these accounts based on different stages of life and goals:

Young Professionals

Prioritize TFSA for flexibility, short-term goals, and tax-free growth

Consider FHSA if homeownership is a goal

Mid-Career Individuals

Maximize RRSP contributions to reduce taxable income in higher tax brackets

Use TFSA for supplementary savings with future tax-free access

Plan RRSP withdrawals strategically to manage potential withholding taxes

First-Time Homebuyers

Combine FHSA and RRSP (through the Home Buyers' Plan) to maximize down payment potential

Supplement with TFSA for additional flexibility

Retirement Planners

Maintain regular RRSP contributions for long-term growth and immediate tax benefits

Use TFSA for tax-free retirement income to complement RRSP withdrawals

Develop RRSP withdrawal strategy to minimize the impact of withholding taxes and overall tax liability

Pro Tips for Maximizing Your Accounts

Financial planning isn't about perfection—it's about progress. These tax-advantaged accounts are powerful tools, but the most important investment is your understanding and consistent strategy. As you navigate your financial journey, keep these key principles in mind:

1. Understand Your Personal Tax Situation

Contributions impact differently based on income

Consider consulting a financial advisor

2. Don't Treat Accounts in Isolation

View them as complementary tools

Balance between immediate flexibility and long-term goals

3. Regular Review and Rebalancing

Reassess your strategy annually

Adjust contributions based on life changes

Your financial journey is unique. What works for others might not be your ideal path. The goal is not to follow a universal blueprint, but to create a strategy that aligns with your personal financial aspirations and lifestyle.

Looking for a Korean version of this post? Click Here

Content & Graphic Design by Chaasy Design / Content Collaboration with Chloe Lee

[VOL.008] Accelerating Financial Growth with Strategic Leveraging

Explore how strategic leveraging can fast-track financial goals with tax efficiency, investment opportunities, and disciplined savings. Learn who benefits and build your tailored strategy today!

In the world of wealth management, time is often considered your greatest ally. While the magic of compounding requires patience, what if you could shorten this journey and achieve financial success even faster?

Leveraging is an investment strategy that allows you to borrow money to invest, thereby enhancing potential returns and helping you reach your financial goals more swiftly. Though the concept may seem daunting at first, leveraging can be both effective and manageable when approached with the right guidance.

What is Strategic Leveraging?

At its essence, leveraging means utilizing borrowed money to make investments. By accessing capital beyond personal savings, you can aim for higher returns. While this might sound complex, the principle is similar to buying a house with a mortgage – you're using borrowed money to invest in an asset that has the potential to grow in value over time.

However, it requires an understanding of both the investment landscape and the risks involved, making it essential to approach this strategy with care and precision.

Why Consider Leveraging in Your Financial Strategy?

The appeal of leveraging lies in its potential to amplify your investment returns. However, it's not just about potential gains. When structured properly, leveraging can offer several strategic advantages.

Tax Efficiency

One of the most compelling benefits of leveraging is the potential to deduct interest on loans used for investment purposes. According to the Canada Revenue Agency (CRA), interest on such loans can generally be deducted if the borrowed funds are used to generate income like dividends or interest. However, staying informed about evolving tax laws is critical to maximizing this benefit.

Enhanced Investment Opportunities

Leveraging can open doors to investment opportunities that might otherwise be out of reach. It allows you to:

Diversify your portfolio more broadly

Take advantage of timely investment opportunities

Access sophisticated investment strategies typically reserved for larger portfolios

Who Should Consider Strategic Leveraging?

Leveraging isn't a one-size-fits-all solution, but it can be particularly valuable for:

High-Income Earners: High-income individuals often face limitations on their Registered Retirement Savings Plan (RRSP) contributions. Leveraging provides an opportunity to invest beyond these constraints, enabling broader financial growth.

Investors with Non-Registered Portfolios: Those investments outside of registered accounts, along with non-deductible debts such as mortgages or car loans, can strategically leverage their situation to optimize tax savings.

Holders of Permanent Life Insurance: By combining a permanent life insurance policy with a leverage loan, clients can benefit from tax-deductible insurance premiums and defer capital gains taxes upon death.

Small Business Owners: Business owners looking to remove retained earnings from their companies can leverage these funds to invest in a tax-efficient manner, mitigating substantial tax bills.

New Investors: For individuals beginning to take savings seriously, leveraging can represent an advantageous option. With a long-term investment horizon, new investors can take advantage of compounding effects while the obligation of loan repayments can help establish a disciplined savings habit.

Building a Strategic Leveraging Plan

The key to successful leveraging lies in careful planning and execution:

Step 1: Assessment

Work with a financial planner to evaluate your:

Risk tolerance

Cash flow stability

Investment objectives

Time horizon

Step 2: Strategy Development

Create a comprehensive plan that includes:

Investment selection

Risk management measures

Tax optimization strategies

Regular monitoring and rebalancing protocols

Step 3: Implementation and Monitoring

Execute your strategy with regular reviews to ensure it continues to align with your financial goals and market conditions.

Is Leveraging Right for You?

Strategic leveraging can be a powerful tool for accelerating wealth building, but it's not suitable for everyone. Success requires careful consideration of key factors. Market fluctuations, interest rate changes, and ongoing repayment obligations create inherent risks that must be managed through:

A clear understanding of the strategy

Comfort with taking calculated risks

Strong cash flow management

A long-term perspective

Professional guidance

Moving Forward with Confidence

If you're considering leveraging as part of your financial strategy, the key is to start with a thorough understanding and professional guidance. Remember, the most successful investment strategies are those that align with your personal financial goals, risk tolerance, and long-term objectives. Contact us to learn more about how strategic leveraging might fit into your wealth-building journey.

Looking for a Korean version of this post? Click Here

Content & Graphic Design by Chaasy Design / Content Collaboration with Chloe Lee

[VOL.007] Mastering Tax Planning in Canada

Discover the keys to effective tax planning in Canada. Learn strategies to minimize liabilities, maximize deductions, and optimize your financial future with expert guidance.

Tax planning is a cornerstone of financial stability, yet it often gets overlooked. By effectively managing your taxes, you can reduce liabilities, increase savings, and redirect those funds toward investments that build your future wealth.

This guide highlights the importance of tax planning and provides practical insights tailored to diverse financial situations. Whether you’re looking to optimize savings, navigate Canada’s tax system, or secure long-term financial goals, proactive tax strategies can make a lasting difference.

The Fundamentals of Canadian Tax Planning

To make the most of your tax planning strategies, a clear understanding of how the tax system works is essential. In Canada, the progressive tax system, administered by the Canada Revenue Agency (CRA), is designed so that higher income results in higher tax rates.

The system includes both federal and provincial income taxes. Federal taxes are applied across several income brackets to fund national expenditures, while each province, including British Columbia, sets its own tax brackets and rates. These provincial rates are subject to annual adjustments, such as changes in the number of brackets or threshold amounts.

To simplify the complexity of separate tax structures, combined income tax rate tables provide a clear overview of total rates for each income level. The graph below illustrates the 2024 federal and provincial tax brackets for British Columbia, showcasing how marginal tax rates apply to different levels of taxable income.

Why Tax Planning is a Game-Changer

Taxes are a fact of life, but how you manage them can make a significant difference in your financial future.

Effective tax planning empowers you to:

Reduce Your Tax Burden: By taking advantage of tax-saving opportunities, you can lower your taxable income and keep more of your earnings.

Maximize Government Benefits: Many programs, such as the Canada Child Benefit (CCB) or GST/HST refunds, offer valuable financial relief.

Optimize Your Investments: Tax-advantaged accounts like RRSPs and TFSAs allow your money to grow tax-free or tax-deferred, improving returns over time.

Increase Financial Security: Managing taxes strategically ensures your resources are working efficiently to support your long-term goals.

Who Benefits from Tax Planning

Tax planning isn’t just for the wealthy—it’s for everyone. No matter your income level or life situation, tailored strategies can help you maximize financial benefits.

High-Income Earners (T4)

For professionals and executives, tax planning can make a substantial impact:

RRSP Contributions: Reduce taxable income and potentially increase your tax refund.

RRSP Loans: Use loans to maximize RRSP contributions and gain immediate tax relief.

FHSA Contributions: Save for your first home with tax-deductible contributions.

Investment Loans: Deduct interest on eligible loans to lower your tax bill.

Families with Young Children

Families can reduce their tax burden while planning for the future:

Canada Child Benefit (CCB): Receive tax-free payments of up to $648 to support child-related expenses.

Spousal RRSP Contributions: Split income in retirement to lower overall taxes.

Childcare Subsidy: Access up to $1,250 to help cover daycare costs.

RESP Contributions: Save for your children’s education with government grants.

GST/HST Refund: Qualify for direct financial relief through refundable tax credits.

Post-Secondary Students

Students can start building their financial foundation early:

Tuition Tax Credits: Offset future taxes by keeping track of tuition payments.

GST/HST Refunds: Ease financial strain with annual refunds, including up to $519.

TFSA Contributions: Begin investing with tax-free growth potential.

Low-Income Earners

Even with modest income, tax planning offers opportunities to improve financial health:

Canada Workers Benefit (CWB): Access refundable tax credits for additional support with up to $2,616.

GST/HST Refunds: Benefit from direct cash refunds to boost cash flow.

The Hidden Cost of Taxes on Investments

Tax planning extends beyond income; it also protects your investments. Without proper strategies, taxes can severely erode long-term returns. For example, a $1 investment growing to $1,048,576.00 without taxes could shrink dramatically with a 40% tax rate ($12,089.26). Refer to the graph below and click the arrow to clearly see the difference for yourself.

Have you noticed the striking difference? It’s a challenge many investors face, but the good news is that there are effective strategies to overcome it.

Using tax-advantaged accounts like RRSPs and TFSAs allows your investments to grow without the drag of taxation, significantly boosting your long-term financial outcomes.

Take the Next Step

Tax planning isn’t a one-time activity—it’s an ongoing process that evolves alongside your financial situation. By taking a proactive approach, you can minimize what you owe, keep more of your hard-earned income, and align your taxes with your long-term financial goals.

As tax laws are constantly evolving, staying informed about these changes allows you to make decisions that optimize your financial outcomes. Working with a financial planner or tax specialist can help uncover overlooked opportunities and ensure your strategies remain effective.

Start small, but start now—building these habits today will lead to greater financial resilience in the future.

Looking for a Korean version of this post? Click Here

Content & Graphic Design by Chaasy Design / Content Collaboration with Chloe Lee

[VOL.006] Navigating Economic Uncertainty: Wealth Strategies to Counter Inflation

Discover a holistic approach to financial planning with the Financial Planning Pyramid. This blog explains how to build a strong financial foundation by addressing key areas like emergency savings, investments, tax strategies, retirement, and estate planning.

In today’s dynamic economic environment, protecting and growing wealth amid persistent uncertainty has become increasingly complex. Global markets remain volatile, with rapidly shifting economic indicators often requiring a reassessment of traditional investment strategies. For Canadians, these dual pressures of market fluctuations and economic unpredictability emphasize the importance of adopting practical and systematic wealth management approaches.

To address these challenges, implementing strategic wealth preservation techniques and investment strategies tailored for volatile conditions is essential. In this post, we delve into the impact of inflation and explore how consistent approaches like dollar-cost averaging can enhance portfolio resilience, providing actionable strategies for achieving long-term financial stability.

Inflation: Safeguarding Your Wealth

Inflation gradually erodes the purchasing power of your money, impacting everything from daily expenses to long-term savings and investments. Over the past 20 years, Canada Inflation Rate has fluctuated significantly, ranging from a high of 6.8% in 2022—driven by global economic pressures—to periods of near-zero inflation, such as in 2009 and 2015 during major economic downturns. Being aware of its effects and adopting proactive strategies is essential for maintaining financial stability.

How Inflation Affects You

Purchasing Power: Inflation reduces what your money can buy over time. For instance, $100 today may have less value in a few years, underscoring the importance of investments that outpace inflation.

Interest Rates: Rising inflation typically drives up interest rates, making mortgages and loans more costly. Homeowners with variable rates may see increased payments, while rent can also climb as landlords adjust to higher expenses.

Budgeting Challenges: Inflation adds unpredictability to future costs, making it harder to plan for goals like retirement or education.

Wealth Preservation Strategies

Diversify Your Portfolio: A blend of stocks, bonds, real estate, and other assets can help balance returns and manage inflation risk.

Upskill and Increase Income: Negotiating for wage increases or advancing your skills can help you keep pace with living costs.

Strategic Savings: Consider laddering your savings across high-interest accounts or short-term investments to maximize returns while maintaining access to cash.

Dollar-Cost Averaging (DCA): A Consistent Investment Strategy

Dollar-cost averaging (DCA) is a steady, low-stress investment approach that involves investing a fixed amount at regular intervals, regardless of market conditions. Unlike lump-sum investing, DCA helps smooth out market fluctuations by spreading investments over time, making it particularly advantageous for long-term investors.

For example, instead of investing $1,000 at once, DCA suggests investing $200 monthly over 5 months. This method helps buy more shares when prices are low and fewer when prices are high, effectively averaging your cost per share. This approach can be especially beneficial in volatile markets, helping investors stay focused on their long-term goals without reacting emotionally to short-term shifts.

While DCA doesn’t guarantee higher returns, it promotes consistent investing, reducing decision fatigue and market timing pitfalls. This systematic approach empowers investors to build wealth with confidence and clarity, making DCA an effective choice for those aiming for gradual wealth accumulation.

Building Financial Resilience: From Strategy to Action

The impact of inflation on personal wealth remains a critical consideration for every Canadian investor. While inflation presents challenges, it also creates opportunities for those who approach it strategically. By implementing a diversified investment approach, maintaining consistent investment practices through DCA, and actively managing your income potential, you can build a robust defense against inflation's erosive effects.

As markets evolve and economic conditions shift, staying informed and regularly reviewing your financial strategy will be key to maintaining and growing your wealth in real terms. Remember that wealth preservation is not about finding a single perfect strategy but creating a balanced, adaptable approach that aligns with your long-term financial goals. It's crucial to clearly assess your financial situation, objectives, and risk tolerance to find the most suitable approach for you.

DIEM is here to help you effectively navigate this process. Take action today to secure your financial tomorrow—your future self will thank you for it.

Looking for a Korean version of this post? Click Here

Content & Graphic Design by Chaasy Design / Content Collaboration with Chloe Lee

[VOL.005] Building a Strong Financial Foundation: A Holistic Approach to Wealth Management

Build a resilient financial future with a holistic wealth management approach. This blog introduces the Financial Planning Pyramid, covering key aspects like emergency funds, risk management, investments, tax strategies, retirement, and estate planning.

The path to lasting financial success requires more than just smart investments. While many focus exclusively on market returns, true wealth management encompasses a broader spectrum of financial planning elements that work together to create lasting prosperity.

A well-structured financial strategy integrates emergency planning, risk management, tax optimization, and estate planning alongside traditional investment approaches. This comprehensive framework not only provides stability during market fluctuations but also establishes the foundation needed for sustained wealth accumulation and preservation across generations.

The Financial Planning Pyramid: A Blueprint for Financial Security

The Financial Planning Pyramid provides a systematic approach to building this holistic strategy, emphasizing the importance of establishing strong fundamentals before pursuing more advanced financial objectives. Each layer of the pyramid serves a distinct purpose while supporting the levels above it, creating an interconnected system that adapts to changing financial circumstances and goals.

Financial Position

At the foundation of the pyramid is your financial position, which includes emergency savings, debt management, and liquidity. This layer emphasizes the need for accessible cash reserves to cover unexpected expenses, ensuring financial stability without relying on credit or liquidating investments.

Risk Management

Next is risk management, which protects against setbacks caused by unforeseen events. Having the right insurance—such as life, health, and disability—creates a safety net that allows you to maintain stability through challenging times without compromising your long-term goals.

Wealth Accumulation

With a secure financial base, you can shift focus to wealth accumulation. Here, you explore investment options like employer-sponsored retirement plans, insured retirement accounts, and taxable investment accounts. Portfolio diversification and risk alignment are critical at this stage to maximize growth potential while staying aligned with your goals.

Tax Planning

Tax planning is an essential element that enhances the effectiveness of every layer in the pyramid. Strategic tax management can increase the efficiency of your financial plan, affecting both growth and wealth preservation. Incorporating tax considerations early on can yield benefits over time.

Retirement Planning

Retirement planning becomes more central as you advance financially, involving detailed strategies for generating sufficient retirement income. This includes planning anticipated expenses, managing retirement accounts, and understanding the implications of government benefits like OAS (Old Age Security) and CPP(Canada Pension Plan).

Estate Planning

At the top of the pyramid is estate planning, which ensures assets are distributed according to your wishes. This layer encompasses more than just a will; it includes beneficiary designations, medical directives, and potential trusts, providing for efficient transfer of wealth while considering potential tax impacts for beneficiaries.

Beyond the Pyramid: Integrating Financial Success

The financial planning pyramid serves as more than just a theoretical framework—it represents the interconnected nature of wealth management. Each layer builds upon and reinforces the others, creating a dynamic system that evolves with your financial journey. Understanding these relationships enables more effective decision-making and resource allocation across all aspects of your financial life.

The true power of holistic wealth management lies in its ability to address both immediate needs and long-term aspirations. By maintaining focus on all elements of the financial pyramid simultaneously, you create a resilient financial structure capable of weathering market volatility, life changes, and economic uncertainties. This comprehensive approach ensures that your wealth management strategy remains aligned with your goals while adapting to changing circumstances and opportunities.

Moreover, the pyramid framework emphasizes the importance of sequential development in financial planning. Just as a physical pyramid requires a solid foundation to support its upper levels, your financial strategy must be built on stable ground. This methodical approach helps prevent the common pitfall of pursuing advanced investment strategies before establishing fundamental financial security.

As markets evolve and financial products become increasingly complex, maintaining this holistic perspective becomes even more crucial. It allows you to evaluate new opportunities within the context of your overall financial structure, ensuring that decisions enhance rather than compromise your financial stability. This balanced approach to wealth management provides the framework needed to build and preserve wealth effectively across generations.

Looking for a Korean version of this post? Click Here

Content & Graphic Design by Chaasy Design / Content Collaboration with Chloe Lee

[VOL.004] The Secret to Wealth-Building: Unlocking the Power of Time

Discover the secret to wealth-building by leveraging time. Learn how starting early, understanding compound interest, and applying the Rule of 72 can dramatically enhance your financial growth.

In today's economic landscape, Canadians face mounting financial strain - from persistent inflation and soaring housing costs to the challenge of living paycheck to paycheck. While these pressures can make planning for the future seem daunting, they actually underscore the critical importance of strategic financial planning. The key lies not in finding a universal solution, but in developing a personalized approach that addresses your unique circumstances and goals.

Financial independence begins with mastering fundamental concepts. This knowledge serves as your foundation, enabling you to evaluate your current position, identify opportunities for growth, and craft strategies that align with both personal and professional financial objectives. Without these essential principles, you might miss crucial opportunities for building long-term wealth and financial security.

By understanding and applying these core concepts, you can create a robust financial plan that not only provides stability but also adapts to life's changes, giving you the confidence to navigate any financial challenge.

The Power of Starting Early: Time is Your Greatest Asset

The most compelling principle in wealth-building is the impact of time. The earlier you start saving and investing, the greater your money's growth over time. This growth is driven by compound interest, where your investment’s interest generates its own earnings.

Consider this: investing $2,000 annually from ages 22 to 27 can yield significantly more retirement savings than investing the same amount from ages 28 to 62. This dramatic difference stems from compound growth - your money grows not just from your initial investment, but from years of accumulated returns. The power of this effect will become clearer in the graph that follows.

The impact of early investing becomes even more crucial when considering today's retirement needs. BMO's 13th Annual Retirement Study revealed that Canadians now estimate they need $1.7 million to retire, a 20% increase from the $1.4 million reported in 2020. This rising benchmark emphasizes the urgency of early action. While delaying savings limits your growth potential, starting early - even with modest contributions - leverages time to build substantial wealth.

Understanding Rate of Return: Your Growth Catalyst

Your investment's rate of return fundamentally impacts your wealth-building journey. Higher returns can boost growth, but they often come with increased risk. The goal is to strike a balance that aligns with your objectives.

The Rule of 72 offers a practical way to understand investment growth. By simply dividing 72 by your expected annual return rate, you get a rough estimate of how many years it will take for your investment to double in value. For example, if you're expecting a 6% annual return, this calculation shows that your investment would likely double in about 12 years (72 ÷ 6). The graph below demonstrates the Rule of 72 in action, showing how investments grow at different annual return rates—3%, 6%, and 12%.

In financial planning, understanding the Rule of 72 is essential for several reasons:

Setting Realistic Goals: Knowing the timeline for investment growth allows you to set achievable financial goals, like saving for retirement, a home, or other major milestones.

Encouraging Early Investment: The longer your money is invested, the more compounding can enhance your future wealth. Delaying investments limits the long-term growth of your savings.

Evaluating Investment Options: Applying the Rule of 72 helps evaluate different opportunities and make informed choices based on risk tolerance and goals.

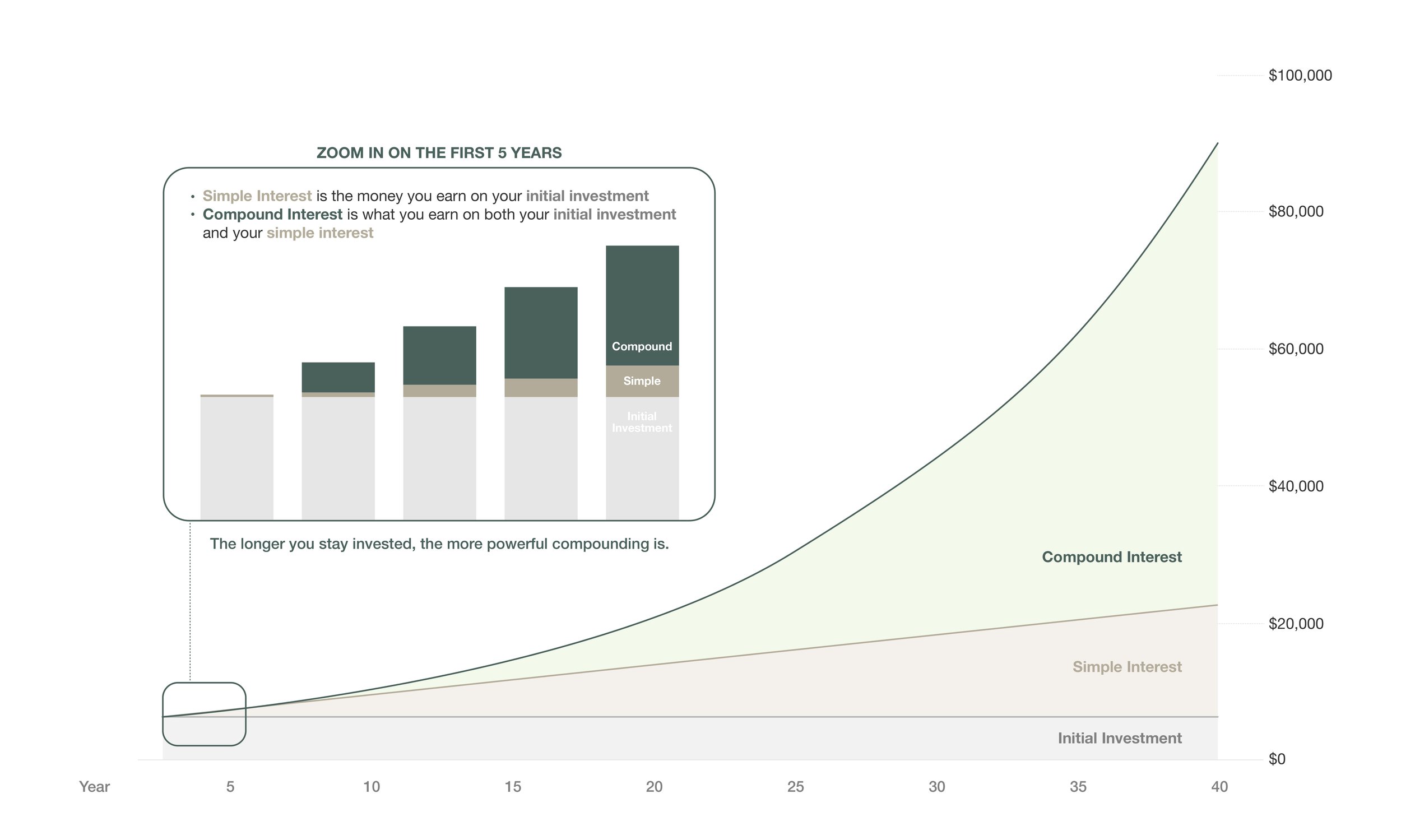

The Rule of 72 becomes even more powerful with compound interest, as interest earned compounds over time, resulting in exponential rather than linear growth. To illustrate this dramatic difference, consider a single investment of $6,000: With simple interest at 7% annually, your money grows steadily but modestly. However, with compound interest at the same rate, that $6,000 could grow to approximately $90,000 over 40 years – a striking demonstration of earning money on the money you earn. Looking at the graph below, you can see this remarkable contrast between simple and compound interest, where the compound interest line curves upward dramatically while simple interest follows a straight path.

Your Financial Success Starts Now

A financial plan tailored to your unique needs does more than provide stability; it enables you to seize opportunities and face future uncertainties with confidence. The principles covered today – early investing, compound interest, and the Rule of 72 – serve as stepping stones to financial freedom. While the current economic climate may present challenges, these fundamentals are powerful tools for building lasting wealth. Remember, it’s not about how much you start with, but how soon you begin.

Looking for a Korean version of this post? Click Here

Content & Graphic Design by Chaasy Design / Content Collaboration with Chloe Lee